The cornerstone of the EU’s policy to combat climate change is the EU Emissions Trading System (EU ETS). Various economic sectors (e.g. power, heat, manufacturing industries, maritime, aviation) have been included within this cap-and-trade system to incentivise CO2 reduction within each sector, or through trading of allowances with other economic sectors included in the EU ETS where emission reduction costs are lower.

Aviation and the EU ETS

The EU decided to include aviation within the EU ETS in 2008, and the system has been applied to aviation activities since 2012. As such, they are subject to the EU's greenhouse gas emissions reduction target of at least minus 55% by 2030 compared to 1990. The scope of the EU ETS applies to flights within and between countries in the European Economic Area, as well as departing flights from EEA to Switzerland and to the United Kingdom, while ICAO CORSIA applies for flights to and from third countries.

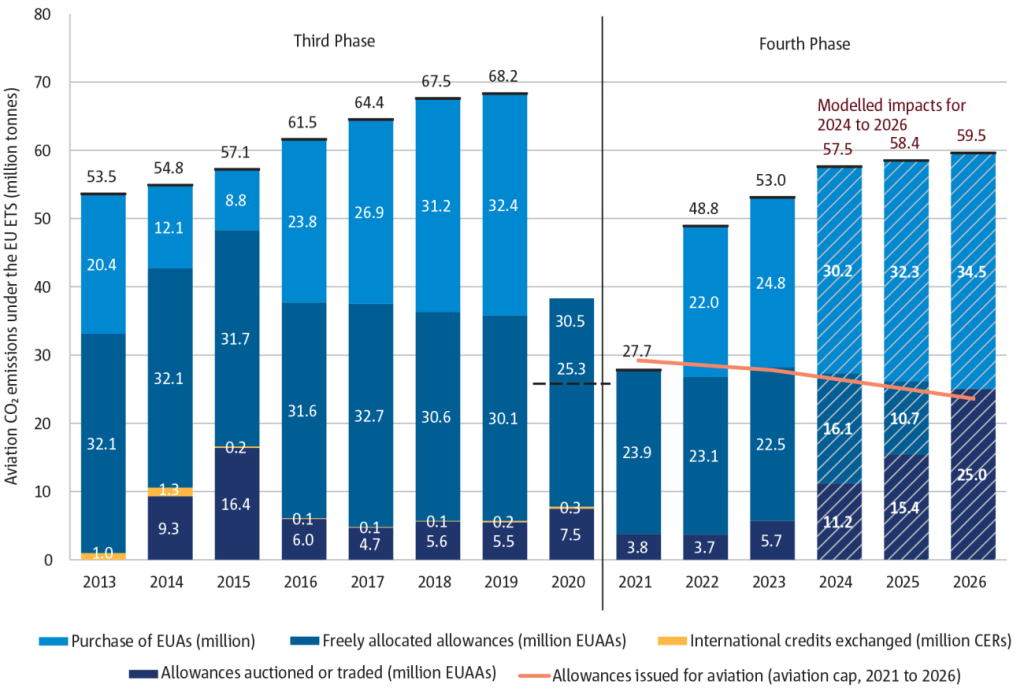

Historic and forecasted aviation emissions under EU ETS

The initial total amount of aviation allowances within the EU ETS in 2012 was 95% of the average annual emissions between 2004 and 2006 of flights within the full ETS applicability scope (all flights departing from or arriving in the European Economic Area), representing 221.4 million tonnes (Mt) of CO2 per year. Flights to and from airports in non-EEA countries or in the outermost regions were subsequently excluded until the end of 2023 through a temporary derogation. This exclusion facilitated the negotiation of the CORSIA scheme at the International Civil Aviation Organisation (ICAO). The EUAAs issued for aviation activities in the ETS's third phase (2013-2020) was adjusted for the applicability scope. While aircraft operators may use EUAAs as well as EU Allowances (EUAs) from the stationary sectors, stationary installations are not permitted to use EUAAs. In addition, aircraft operators were entitled to use certain international credits (CERs) until 2020 up to a maximum of 1.5% of their verified emissions. In 2023, there were 254 aircraft operators reporting a total of 53 million tonnes (Mt) of CO2 emissions under the EU ETS.

Aviation CO2 emissions under the EU ETS in 2013-2023 and modelled impact of the revised ETS Directive for years 2024-2026, where 1 EUAA / EUA equals 1 tonne of CO2 emissions

Note: Data reflects the years in which the EUAAs were effectively released to the market. This applies especially for allowances attributable to years 2013, 2014 and 2015, which were all auctioned in 2015. The 2014 auctions of EUAAs relate to auctioning of EUAAs due to the postponement of 2012 auctions. Modelled data for years 2024-2026 from the updated AERO-MS model. In addition, the Swiss (CH) ETS is forecast to result in a purchase of ETS allowances by aviation sector as follows: 0.3 million in 2023; 0.4 million in 2024; 0.5 million in 2025 and 0.6 million in 2026.

Aircraft operators are required to report verified emissions data from flights covered by the scheme on an annual basis.

The total verified CO2 emissions from aviation covered by the EU ETS increased from 53.5 Mt in 2013 to 68.2 Mt in 2019 (see Figure above). This implies an average increase of CO2 emissions of 4.15% per year. The impact of the COVID-19 pandemic on international aviation saw this figure fall to 25.3 Mt in 2020, representing a decrease of 63% from 2019 levels. From 2013 to 2020, the average amount of annual EUAAs issued was around 38.3 Mt of which about 15% have been auctioned by the Member States, while 85% have been allocated for free. The purchase of EUAs by the aviation sector for exceeding the EUAAs issued went up from 20.4 Mt in 2013 to 32.4 Mt in 2019 contributing thereby to a reduction of around 155.6 Mt of CO2 emissions from other sectors during 2013-2019. As a result of the COVID-19 pandemic, the verified emissions of 25.3 Mt in 2020 were below the freely allocated allowances for the first time.

Since 2021, a gradual recovery of aviation activities has been observed: total verified aviation CO2 emissions covered by the EU ETS in 2021, 2022 and 2023 were 27.7 Mt, 48.8 Mt and 53.0 Mt respectively. The free allowances allocated to the aviation sector were 23.9 Mt in 2021, 23.1 Mt in 2022 and 22.5 Mt in 2023. Following the rebound of aviation sector’s CO2 emissions from the COVID-19 pandemic, the sector became a net purchaser of EUAs again in 2022 (22.0 Mt) and in 2023 (24.8 Mt). From 2021 until 2023, a linear reduction factor of 2.2% has been applied to the Allowances issued for aviation, and this factor will increase to 4.3% for the period of 2024-2027.

The modelled CO2 emissions under the aviation ETS are expected to grow to 59.5 Mt in 2026 (Modelling by EASA AERO-MS model). In line with the gradual phase out of the free allowances to the aviation sector by 2026, the annual amount of freely allocated EUAs for aviation is expected to reduce from 16.1 Mt in 2024 to 10.7 Mt in 2025 and then become zero from 2026 onwards. Purchase of EUAs is expected to grow from 30.2 Mt in 2024 to 34.5 Mt in 2026. Emissions benefits from the claiming of Sustainable Aviation Fuels (SAF) could grow from 0.5 Mt in 2024 to 1.7 Mt in 2026, assuming a zero emissions factor of SAF as per the EU ETS Directive. Moreover, there could be a relative demand reduction within the aviation sector over the years 2024-2026 of 9.8 Mt as a result of the carbon price incurred due to the EU ETS.

The annual average EU ETS carbon price varied between €4 and €30 per tonne of CO2 during the 2013-2020 period. Consequently, total aircraft operator costs linked to purchasing EU Allowances (EUAs) have gone up from around €84 million in 2013 to around €955 million in 2019. Since 2021, the EUA price has increased significantly, reaching average annual EUA prices of more than €80 in 2022 and 2023, resulting in total aircraft operator cost of approximately €1.8 billion in 2022 and €2.1 billion in 2023. Peak EUA prices exceeding €90 per tonne of CO2 were observed in early 2022 and again in 2023. For the period of 2024-2026, it is estimated that the ETS cost could represent approximately 4-6% of airlines’ total annual operating costs.

From 2024 until 2030, airlines can apply for additional ETS allowances to cover part or all of the price differential between the use of fossil kerosene and SAF on their flights covered by the EU ETS. A maximum amount of 20 million allowances will be reserved for such a support mechanism, and airlines can apply for an allocation on an annual basis. The Commission will calculate the price differentials annually, taking into account information provided within the ReFuelEU Aviation Annual Technical Report from EASA. An initial 1.3 million allowances under this support mechanism were allocated to eligible airlines in September 2025.

Review of EU ETS and CORSIA in 2026

The EU Commission continuously monitors the developments at the ICAO negotiations and will report in 2026 on the progress at ICAO on the implementation of the CORSIA scheme as well as on CORSIA’s environmental performance, accompanied by legislative proposals to amend the EU ETS Directive, where appropriate.

European Model for Impact Assessments of Market-based Measures

The EASA AERO Modelling System (AERO-MS) has been developed to assess the economic and environmental impacts of a wide range of policy options to reduce international and domestic aviation GHG emissions. These policies include taxes (e.g. fuel and ticket taxation), market-based measures (e.g. EU ETS, CORSIA), as well as the introduction of sustainable aviation fuels and air traffic management improvements. The model can provide insight into the effect of policy options on both the supply side and demand side of air travel due to higher prices, and the forecasted impact on emission reductions.

The EASA AERO Modelling System (AERO-MS) has been developed to assess the economic and environmental impacts of a wide range of policy options to reduce international and domestic aviation GHG emissions. These policies include taxes (e.g. fuel and ticket taxation), market-based measures (e.g. EU ETS, CORSIA), as well as the introduction of sustainable aviation fuels and air traffic management improvements. The model can provide insight into the effect of policy options on both the supply side and demand side of air travel due to higher prices, and the forecasted impact on emission reductions.

During the last 20 years, the AERO-MS has been a key part of more than 40 international studies where the model results have informed policy discussions and decisions. Beneficiaries of the AERO-MS include a wide range of organizations, including the European Commission, Member States, EASA, IATA, ICAO, aviation industry and NGOs. As a part of a project funded by the EU Horizon 2020 research programme, an update to AERO-MS was completed in 2024 to enhance its capabilities for future studies. This included a new base year of 2019 traffic and emissions, latest information on price elasticities, the addition of particulate matter emissions modelling and the inclusion of the impacts of SAF.